Under the Income tax Act, 1961 assessee is required to maintain books of accounts. Assessee can maintain books of accounts under cash basis or mercantile basis of accounting. Assessee should consistently follow the method of accounting. The Central Government had via power given in section 145(2) notified Income Computation and Disclosure Standards. ICDS-II deals with valuation of Inventories. IF there is deviation from any ICDS notified under section 145(2) then effect should be reported in form 3CD audit report . The article gives the brief about section 145, 145A & ICDS-II with examples.

Valuation of Inventories under Income tax Act, 1961

Introduction

Under the Income tax Act, 1961 assessee is required to maintain books of accounts. Assessee can maintain books of accounts under cash basis or mercantile basis of accounting. Assessee should consistently follow the method of accounting. The Central Government had via power given in section 145(2) notified Income Computation and Disclosure Standards. ICDS-II deals with valuation of Inventories. IF there is deviation from any ICDS notified under section 145(2) then effect should be reported in form 3CD audit report. The article gives the brief about section 145, 145A & ICDS-II with examples.

Method of accounting.

There are two method of accounting

2. Mercantile Basis

ICDS-II – Valuation of Inventories

Disclosure:

The accounting policies adopted in measuring inventories along with the total carrying amount of inventories should be disclosed in the financial statements.

Valuation:

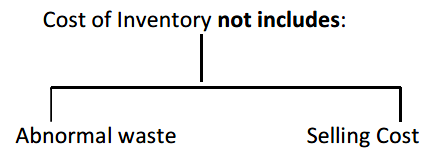

Inventories shall be valued at cost, or net realizable value, whichever is lower

Cost of inventories shall be assigned by using the First-in First-out (FIFO) or weighted average cost.

Net realizable value:

Net realizable value (NRV) is the value of an asset that can be realized upon the sale of the asset, less a reasonable estimate of the costs associated sale of the asset.

Notes:

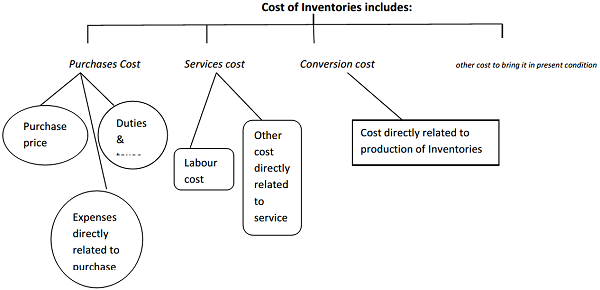

Trade discounts, rebates, etc. will not be included in the cost of Purchases.

Administrative overheads that do not bring the inventories to their present condition are excluded.

Storage costs, unless those costs are necessary in the production process prior to a further production stage are excluded.

The bare section from the ACT Section 145 & 145A:

Section 145.

(1) Income chargeable under the head “Profits and gains of business or profession” or “Income from other sources” shall, subject to sub-section (2), is computed in accordance with either cash or mercantile system of accounting regularly employed by the assessee.

(2) The Central Government may notify income computation and disclosure standards to be followed by any class of assessees or in respect of any class of income.

(3) Where the Assessing Officer is not satisfied about the correctness or completeness of the accounts of the assessee, or where the method of accounting provided in sub-section (1) has not been regularly followed by the assessee, or income has not been computed in accordance with the standards notified under sub-section (2), the Assessing Officer may make an assessment in the manner provided in Section 144 i.e. Best Judgment Assessement.

Section 145A

For determining the income chargeable under the head “Profits and gains of business or profession”,—

(i) the valuation of inventory shall be made at lower of actual cost or net realisable value computed in accordance with the income computation and disclosure standards notified under sub-section (2) of section 145;

(ii) the valuation of purchase and sale of goods or services and of inventory shall be adjusted to include the amount of any tax, duty, cess or fee (by whatever name called) actually paid or incurred by the assessee to bring the goods or services to the place of its location and condition as on the date of valuation notwithstanding any right arising as a consequence to such payment of taxes fees or cess as the case may be.

Provided further that the comparison of actual cost and net realisable value of securities shall be made category-wise.

Example for Exclusive & inclusive method.

Example. 1

M/S A Associates has opening stock finished goods of Rs.3,00,000/-(Exclusive of GST @ 5%)

During the year 3 items purchased @ Rs.2,50,000/- per item. GST on purchase @ 5%.

2 are sold @ Rs.4,00,000/- per item. GST on sales @ 5%

The Trading Account on “EXCLUSIVE METHOD”

| Particulars | Qty. | Rate | Amount | Particulars | Qty. | Rate | Amount |

| To Opening Stock | 1 | 3,00,000 |

The Trading Account on “INCLUSIVE METHOD”